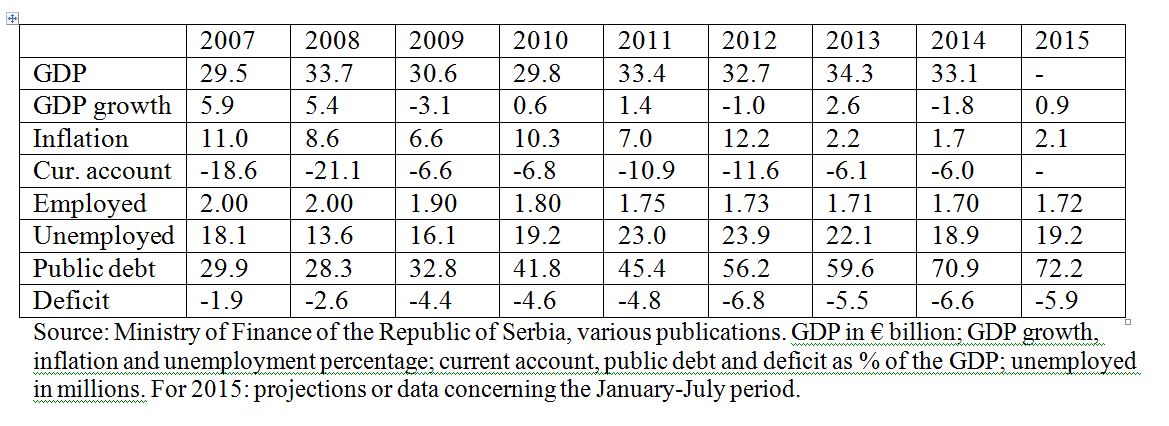

It is with mixed feeling that one can look at Serbia’s basic macroeconomic indicators. Some are featured by good, and some by poor development (Table 1). Those that are improving include inflation, its rate having dropped from over ten percent a few years ago to around 2% in recent years. It is not a good result, but one should bear in mind that monetary stability in Serbia has not been continuous during the past decades. Even when achieved, it does not last long, usually coming at a steep price – as is the case this time, since the National Bank of Serbia has robustly intervened to preserve the exchange rate, whilst keeping interest rates at the 5-12% level at a time when they hovered around 0% in USA and the eurozone.

The development of the current account[1] is favorable, as well; its balance is still negative but it has dropped from over 20% a few years back to around 6% of the GDP in 2014. Import growth is also on the positive side. This exhausts the list of positive trends. The list of negative ones is much longer. National income has been stagnant since 2008. Even if the projected 0.9% growth is realized in 2015, the national income in 2015 will be lower compared to the 2008 one by 0.4pp (percentage points). The number of employees is incessantly decreasing; it has dropped from 2.0 to 1.72 million during the 2008-2014 period. Given the fact that the realized income has remained roughly the same, it can be concluded that the departure of around 280,000 employees has led to increased productivity which would mean that they had represented a surplus, i.e. that they were unnecessary. The unemployment rate has fluctuated in the range between 13.6 and 23.9% with no clear trend.

Table 1: Serbia’s macroeconomic indicators

Serbia’s gravest chronic problem is the incessant public debt growth in light of the stagnant economy. The debt has risen from 28.3% of the GDP in 2008 to 72.2% in mid-2015. As I have written in my previous contribution[2] for the Heinrich Boell Foundation (HBS), Serbia is among two Eastern European countries with the highest-growing public debts, which increases the risk of state bankruptcy. Apart from that, public debt growth has other negative consequences, too, as it indicates higher taxes and lower economic growth in the future. In light of the growing public debt, there is some controversy concerning the budget deficit trend in 2015, which had been one of Europe’s highest in recent years. Serbia is also facing some other economic problems which were not included here, such as population decline, emigration of younger and qualified persons, the country’s growing centralization, growth of the sum of non-performing loans, illiquidity of enterprises, very poor trends in the stock market.

I shall provide two illustrations: The index of the most liquid equities (Belex 15) has dropped from 3,300 points in 2007 to around 650 in 2015. The stock market being the key instrument of the financial market, the previous data gives a clear indication of the business environment in Serbia. Non-performing loans have reached 24% of the total loans (among the three highest rates in Europe) which will be one of the main problems in the years to come. One day, it will shake up the banking system, too, but also public finances, the real sector, even the entire state.

Obviously, good news is outnumbered by problems that cannot be covered in a single text. I will only look back at three issues in the following part.

Firstly, according to official data, the employment rate in Serbia is rising despite the national income declining or stagnating. This seems like an interesting paradox.

Secondly, how much truth is there to the officials’ stating that there had been a sudden decrease of the budget deficit? And how sustainable are the existing results?

Thirdly, it seems as though the International Monetary Fund (IMF) has a positive opinion on the development of economic circumstances and management in Serbia. The question remains, of course, whether such assessment by the IMF is justified.

Taking all into account, one should bear in mind the fact that the debates on these issues are occurring, i.e. assessments are being expressed in a politicized atmosphere, prior to the upcoming local and provincial elections that may be followed by republic elections which, should they be held, would be snap elections. In order to contest these elections, the regime wants to partially alleviate the effects of austerity policies by slightly increasing salaries and pensions, even though austerity is a condition of the Stand-By Arrangement with the IMF. And in order for the IMF to agree with a partial suspension of the austerity measures, certain numbers are required.

Unemployment

Economies can only grow if productivity or the employment rate is increased. Since productivity usually grows at a slow pace, there remains for something to be done in terms of employment. A rise of the employment rate would require a significant increase of investments, which lacks in Serbia. The employment rate in developed countries is around or over 70%, whereas the unemployment rate hovers around 5-10%. In the Balkan countries, things are the opposite – employment rates are low and amount to ca. 50%, whereas unemployment rates are high, usually above 15%, often near 30%. According to data by the International Labor Organization, the 2014 unemployment rates in some of Balkan countries were as follows: Croatia 16.7%, Montenegro 19.0%, Serbia 22.2%, Bosnia and Herzegovina 27.5% and Macedonia 28.2%. High unemployment rates can be used as part of the explanation of the fact that this is Europe’s poorest region where a significant part of the labor force remains unused.

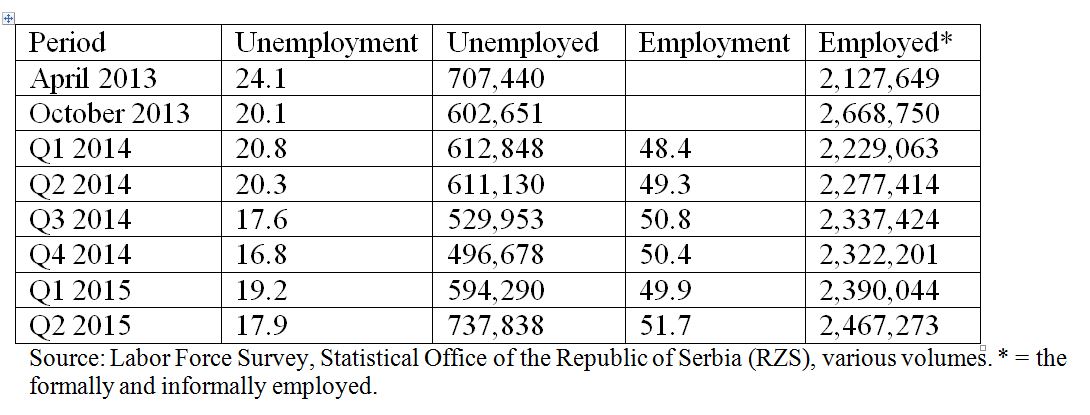

Looking at the quarterly data on employment and unemployment trends in Serbia from early 2013 to June 2015, one notices that unemployment is declining whereas the employment rate is growing. First of all, a few words about the general trend, and then we shall discuss some of the paradoxes.

Between the first and last observed period, unemployment has dropped by 6.2 pp, whereas the employment rate has risen by 3.3 pp (Table 2). This positive trend could change in case of closure of bankrupt enterprises and dismissal of their employees during 2015 and 2016, in which case the unemployment rate would increase by a few percentage points and return to the level of above 20%. It would be ungratifying to prognosticate the numbers pertaining to (un)employment in the months or years to come, as the authorities could decrease the number of enterprises intended for liquidation, and even abandon the closure of bankrupt enterprises and dismissal of employees altogether, primarily due to resistance by interest groups and the looming elections.

Table 2: Employment and unemployment in Serbia, quarterly

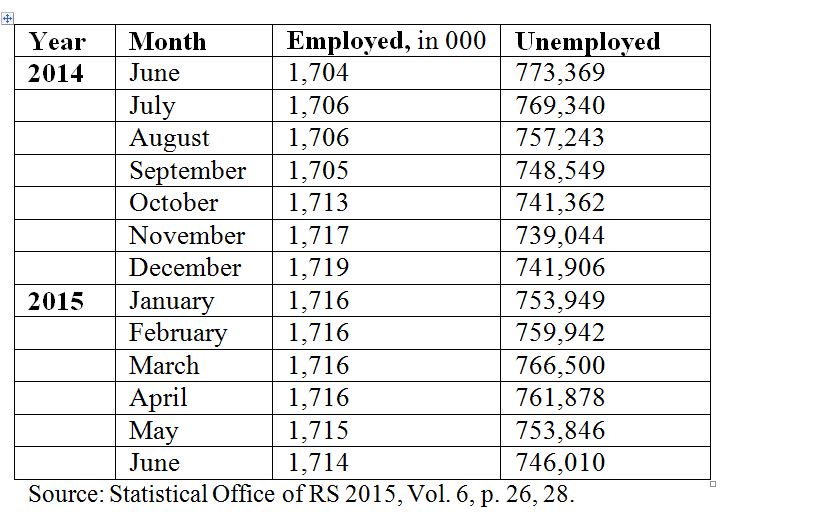

The very trend of the number of employed, i.e. unemployed persons is much more difficult to explain. For instance, the number of unemployed persons has been in a steady decline since April 2013 until the 4th quarter of 2014, by around 210,000. If this can be partly comprehended due to the 2.6% economic growth in 2013, it is difficult to understand such a decline of the unemployment rate in 2014, a year which saw a -1.8% drop in economic activity. It is even more difficult to comprehend the rise of the unemployment rate between the 4th quarter of 2014 and the 2nd quarter of 2015, by around 240,000, as a slight economic growth is expected in 2015. Theory of economics states that the unemployment rate declines during years of growth and rises during years of decreasing economic activity, whereas the trends in said examples run contrary to this apparent economic truth. Similarly, the number of employed persons has been increasing between the 1st quarter of 2014 and 2nd quarter of 2015, by an incredible 240,000. The Labor Force Survey conducted by the Statistical Office of the Republic of Serbia (RSZ) – which is where this data stems from – should be more accurate than the monthly estimates concerning the rates of (un)employment, since the former is done empirically and the latter via models. However, the data from the Labor Force Survey indicate great fluctuations of the number of (un)employed persons, whereas those oscillations are much lower in the case of monthly estimates. Both the surveys and the monthly estimates are being conducted by the same office – the Statistical Office of the Republic of Serbia.

Estimates of the monthly employment and unemployment rates are subject to much greater variations percentage-wise than in terms of absolute numbers. Viewed in absolute figures, the number of employed persons has increased from June 2014 to June 2015 only by 10,000, which is less than 1% of the total number of employed persons, and the total number of the unemployed has decreased during the same period by around 27,000, which amounts to slightly less than 4% (Table 3).

Table 3: Number of employed and unemployed persons in Serbia.

The unemployment rate is obviously dropping faster than the number of employed persons is growing. Reasons behind this can be manifold. For instance, better control of regulations can urge owners of enterprises to ensure legally regular employment of those who have been previously employed in a “grey zone“. The Ministry of Finance claims that the number of informally employed persons has decreased between Q2 2014 and Q2 2015, from 21.2% to 18.5%.[3] Secondly, part of the unemployed persons find seasonal jobs between March and October. Thirdly, the unemployed are more prone, in comparison to employed persons, to seek work abroad. Once he/she moves to another country, an individual is removed from the unemployed list. Fourthly, a similar effect is produced by a partial liberalization of the Labor Law which incites formal employment – insignificantly, but still. Fifthly, a part of the employed persons retire or go abroad and once they are replaced by others, the number of employed persons remains unaltered, but the number of unemployed decreases. Sixthly, there are frequent changes in the methodology and rules of keeping record of the (un)employed, which renders the data hardly comparable in timeline series. Everything considered, the different dynamics of the employment and unemployment rates can somehow be explained.

It is much more difficult to explain the paradox of the decrease in unemployment, i.e. rise in employment during 2014, despite the GDP dropping by 1.8% during that year. The unemployment rate during the observed 6 quarters was at its lowest point (16.8%) in the 4th quarter of 2014. The data on the rise of the employment rate in 2014 is even more drastic if taking into account – instead of the standard Statistical Office series – those contained in the Labor Force Survey, which indicate that the employment rate in 2014 has increased by around 160,000.[4] This increase by some 6.5% has occurred in a year in which the economic activity has dropped by 1.8%. The increase of the employment rate in Q2 2015 as compared to the same period in 2014 seems to be primarily in the public sector – around 16% (24,000) in the education sector, health (15,000) and public administration (13,000). At the same time, there are certain indications (number of paid salaries, retirement, leaving public service...) that the number of employed persons in public administration has decreased: the question arising is which data are credible?

Cross-referencing data on (un)employment with some other ones (tax collection, sectoral trends of economic activity, etc) points out that cases of new employment occur mainly in the public sector, while it seems that there has not been much new employment in the private sector, but mainly the legalization of “grey“ jobs. This goes particularly for sectors with high shares of “grey“ economy, such as tourism, agriculture, civil engineering and services. Data from the Labor Force Survey pertaining to the informally employed shows that their number has not risen, whereas the number of those employed formally has, thus directly confirming the hypothesis on the transfer of a part of the informally employed to regular employment. When this fact or a change in regulations is taken into account as a well-founded general explanation, it is difficult to explain some facts from certain domains of activities: e.g. how did the number of employees in the domain of real estate trading increase by more than 100% between Q2 2014 and Q2 2015, despite the fact that trading in this sector is hardly growing?

The fact that something is wrong with the data indicating a major employment growth – specifically during periods when income is decreasing or stagnant – can be observed in another indirect manner. If the employment rate rises by 10% or more, income should increase dramatically. (It is presumed that productivity remains the same.) Not only is income not growing – it is stagnant or decreasing. Obviously, the described new employment occurs in statistics, but not in reality. Or is it maybe that it was brought about in the loss-producing public sector rather than in the productive private sector. If that is the case, this employment, being unproductive or more precisely harmful, should not have occurred in the first place.

During the next year or two, the (un)unemployment rate trend will be predominantly determined by three factors. Firstly, the development of the economic activity. Even though we have just seen that the short-term lower level of economic activity does not entail a lower employment rate, essentially in normal circumstances, too, a higher level of economic activity entails a higher employment rate and vice versa. Secondly, the pace of bankrupt enterprises’ liquidation: This process’s consistency and pace will also result with a higher unemployment rate. Due to their age and underqualification, those who are still employed with bankrupt state enterprises stand little chance of finding new employment in the private sector (be it in the country or abroad). Of course, if the government suspends the process of liquidation and restructuring, there will be no major decrease of the number of employees. But the state will have to upkeep the unnecessarily excessive spending to subsidize those enterprises through various forms of state assistance. Thirdly, the labor force drain abroad can be a significant factor in the (un)employment statistics, as well. It will be a factor only in case of some major political and economic turmoil in the country, when the wave of emigrants suddenly increases. Basically, the unemployment rate will remain high, certainly above 17%, at times even above 22%. Such high unemployment rate undermines economic growth and prolongs poverty. A significant employment boost requires major improvements of the business climate and rule of law, both of which are currently not on the agenda.

Deficit

Budget deficit has caused for much more public attention than the paradox surrounding (un)employment. There are at least three reasons behind that. Firstly, high deficits in Serbia during the past years have increased the country’s risk of bankruptcy. Secondly, the deficit trend is the basic indicator of fiscal consolidation determining the maintenance of the country’s existing three-year Stand-By Arrangement with the IMF. Thirdly, and finally, it is the deficit trends that the IMF’s approval of the government’s intention to partly return the trimmed pensions and salaries to their previous levels will depend on. This “increase“, again, will mainly influence whether the Serbian Progressive Party (SNS) will call snap republic elections, etc.

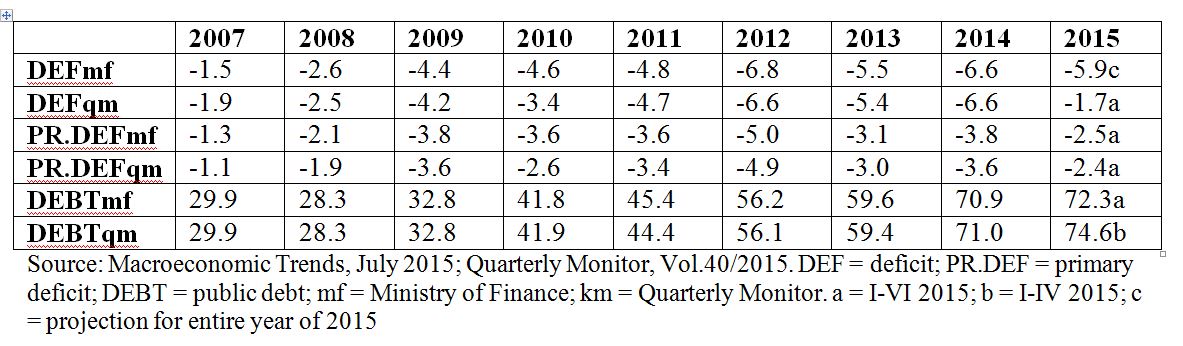

Table 4 contains the data pertaining to deficit and public debt by the Ministry of Finance (mf) and the Quarterly Monitor (qm), respectively. For the most part, they correspond to each other, with the exception of the 2010 deficit. The previous years’ deficits have been high, the first indication of a decrease being 2015.

Table 4: Serbia’s public debt and deficit.

Since the publication of first official data on Serbia’s public revenues, expenditures and balance of payment in 2015, there have been ongoing discussions about the extent to which the situation in public finances had improved and whether it is sustainable. The authorities aimed to show that the situation had improved significantly. Experts pointed out that the situation was better than during the previous period, but not as good as the authorities claim. The volatility of the situation in this field can be observed through the following facts: One of the key indicators used by the authorities is the January-July 2015 deficit which amounted to 39.4 billion dinars (or 34.7% of its last year’s amount), whereas in the same period in 2014 it amounted to as much as 113.5 billion dinars. In the January-August 2015 period, the budget deficit amounted to 44.4 billion[5], and in the same period in 2014 it reached 135.3 billion dinars, i.e. dropped to 32.8% of the last year’s deficit.

The authorities have entered 2015 with a 5.9% deficit prognosis which has thus far proven to be pessimistic. The official version’s pessimism was also contributed to by experts who viewed austerity measures (pension and salary cuts) as the only mechanism to decrease deficit. However, neither the experts nor the state were able to foresee several other developments that have taken place.

Firstly, there was a great influx of non-tax revenues (dividends, license fees, etc) as early as at the year’s beginning, in the amount of ca. 30 billion dinars, whereas it is usual for this type of revenue to arrive either evenly in the course of the year or toward its end. For example, dividend revenues in the first quarter have netted around 17 billion – had it been distributed evenly to all four quarters, the budget would have registered just 4.25 billion in the first.

Secondly, tax and excise revenues have risen, which has been much contributed to by slightly higher collection of VAT (due to the Tax Administration’s pressure on grey economy), introduction of excise duty on electricity and increased excise on tobacco products.

Thirdly, a drop in expenditures for capital investment and severance pay in the amount of ca. 20 billion dinars was recorded during the first four months. In the first 7 months, nearly 47 billion dinars was used for capital expenditures, i.e. 40% of the funds that were allocated for this purpose at the annual level. During the five remaining months of 2015, ca. 70 billion is supposed to be earmarked for capital investments; that is, over 2% of the GDP. Of course, one should not forget about the inflation tax which has increased budget revenues by around 2%.

Basically, due to the circumstances – the important ones having been elaborated in this text – the first quarter has brought much higher revenues, and lower expenditures than expected. As a result, the outlook of public finances was much more favorable at the beginning of this year. During the first four months the deficit only amounted to 22 billion dinars or 1.8% of the four-month GDP. But as the year goes by, things will go back to normal, hence the deficit and debt will rise from the said 1.8% toward 4% or perhaps even higher, which will spoil the existing positive fiscal image. Encouraged by good results in the first quarter, some experts (e.g. the Fiscal Council) have estimated that the budget deficit at the end of 2015 could amount to just 3.5%, although even the FS cites 4.5% as an accurate and sustainable measure.[6] Authors of the Quarterly Monitor were less optimistic: they expect a 4.5-4.7% deficit.[7] Public finances are rigid, both in terms of revenues and expenditures; the established trend is therefore difficult to alter unless major cuts are made. In Serbia’s case, there are none – pension and salary cuts cannot be perceived as such. Of course, there is always the possibility of some new changes. It is expected that by the end of 2015 there will be no major concentrated revenues such as dividends; that capital expenditures will go up and that fatigue will occur in terms of more efficient VAT collection[8], and that a necessity will arise either in form of severance pay (if loss-producing enterprises are to be closed down) or subsidies (if insolvent enterprises keep operating), while interest payments will grow.

The final 2015 deficit is probably to be expected somewhere around 4.0% which is much better than the official 5.9% projection. Should this improvement by any chance come to fruition, it will be mainly due to the pension and salary cuts, more efficient tax collection and a decrease in capital investments. Although the Fiscal Council (2015c) believes the current improvement to be sustainable in the long term, it seems that this is not exactly the case. If pensions and salaries are returned to their previous levels, if tax repression relents, if public enterprises yield lower profits than in 2015 (which is likely), and if the capital expenditures are normalized – a high deficit will reappear, along with the accompanying problems.

With the aforementioned improvement of, say, 4%, it would still be one of the highest deficits in Europe, 1pp above the 3% Maastricht threshold. Even if the improvement is realized, it will impose new indebtedness and the public debt could come close to 80% of the GDP at the end of 2015. Serbia’s debt problem could intensify even if the global price of debt service does not increase, for instance if FED (US Federal Reserve), ECB (European Central Bank) and other globally significant central banks do not raise reference interest rates. Simply put, in case of a constant public debt growth, the creditors will at some point become skeptical as to whether Serbia is capable to service such a high debt and will demand higher yields in order to purchase its debt securities. At this point it is difficult to speculate about the debt amount that might trigger this, nor when it could happen, because such matters depend on the circumstances in the financial market and the creditors’ subjective perception. It goes without saying that the inability to take on more debt would cause Serbia grave consequences. It would require an instant major cut in public finances.

IMF’s Satisfaction?

In November 2014, the Government of Serbia reached an agreement with the IMF on a three-year Stand-By Arrangement in the amount of 1.2 billion euros. The essence of the arrangement is Serbia’s fiscal consolidation, and concrete measures pertain to a decrease of the budget deficit, lowering of salaries in the public sector and state pensions, privatization, reorganization and liquidation of state enterprises, dismissal of surplus employees in the public sector, increased electricity price and introduction of electricity excise, etc. The IMF Board of Directors approved the arrangement with Serbia in February 2015. The first revision was approved in late June 2015 by the IMF, and the second, out of a total of 12 revisions of this arrangement, was carried out in late August 2015. As the IMF mission was leaving Belgrade on September 1st, it was pointed out that the IMF delegation has expressed a positive assessment of the realization of the arrangement’s elements by the Government of Serbia, which has been much publicized by the Serbian media[9]. The question which comes to mind, of course, is how justified is the satisfaction of the IMF?

Based on what was accessible to the media, it seems that the IMF mission was mostly interested in the fiscal dimension of the arrangement. Given the fact that the numbers were better than those outlined in the arrangement’s framework – as we have seen in the previous section – the IMF was seemingly satisfied. A budget deficit significantly lower than expected and pension and salary cuts represent basic elements of fiscal consolidation. The IMF mission would certainly have much less reasons for satisfaction had they observed other parts of the arrangement. Privatization, restructuring and liquidation of bankrupt state enterprises are constantly being postponed, in fact they have not even begun in earnest. Dismissal of surplus employees in the public sector still lacks, as well. On the other hand, it seems that much new employment is being done – particularly in the public sector and particularly when it comes to party staff. The realization of some other, less important parts of the agreement is lagging, as well. Higher electricity prices and introduction of electricity excise seem to be the only tangible achievements.

In such a situation, the IMF mission had a reason for moderate satisfaction, although the indicators of fiscal consolidation will slightly deteriorate by the year’s end – for reasons previously mentioned. However, what probably causes the IMF mission’s concern with regard to Serbia is not this deterioration – because even with it, the deficit will be lower than planned – but rather the demand by the Government of Serbia to recall a part of the austerity measures in order to be able to partly raise salaries and pensions. The amount of this increase is unknown, but it is one the ruling Serbian Progressive Party (SNS) requires in order to call for snap republic elections – the very republic elections that would be called in order to “buy“ more time in power and to improve Vučić’s and SNS’s election result at the local and provincial levels. Republic elections would enable for Prime Minister Vučić to be frontrunner on the ticket which would, in turn, motivate a greater number of SNS supporters to cast their ballots, as he enjoys a higher popularity than any other SNS politician, and the entire SNS, for that matter. According to this calculation, the Progressives would achieve, apart from victory at the republic level, much better results at both local and provincial level.

SNS and Vučić require a “carrot“ of some sort for the elections, and recalling part of the pension and salary cuts is the best solution since it concerns a large number of voters. These cuts must have had arrived at a price for the Progressives in form of a certain drop in popularity, since they are interested in an increase this soon thereafter. The only problem is that a possible partial increase of pensions and salaries would undermine the ongoing fiscal stabilization. The higher the increase, the bigger the potential undermining effect. Should the increase of pensions and salaries account for a third of the late-2014 cut (an amount smaller than that would hardly have a positive political effect expected by the authorities), the effect of budget austerity would drop from 1.1% to 0.7% of the GDP. An eventual amount of the pension and salary increase will be a topic of negotiations between the Government of Serbia and the IMF during the third revision in November 2015. An outcome of the negotiations is uncertain because neither is the IMF principled, nor is the Government of Serbia devoted to reforms and to the arrangement with the IMF.

What is certain is the fact that any significant increase of pensions and salaries would undermine the fiscal consolidation program less than a year since the beginning of its implementation. It would also send a wrong signal to the voters, indicating that the unpleasant period of austerity is over and that it will be followed by further increase of pensions and salaries. Finally, the SNS government could decide in favor of pension and salary increase without the IMF’s consent. It would not be the first time, as something similar took place when as recent as in 2011 the Democratic Party-led government unilaterally terminated the Stand-By Arrangement with the IMF in order to be able to increase state expenditure on the eve of the May 2012 elections. Nevertheless, the Democrats lost that election and Serbia accelerated its indebtedness despite having received a lower credit rating, thereby a more expensive debt service. Termination of the existing arrangement with the IMF could result with similar consequences to Serbian public finances. A difference in comparison with 2011 is a much higher debt level and greater risk of bankruptcy – the debt at the time amounted to around 45%, whereas nowadays it is around 75% of the GDP.

A move such as the increase of pensions and salaries is deeply wrong, yet one that is possible to transpire. We have seen political priorities outweigh economic ones many times. It would be a step in the wrong direction. For, even the present level of austerity and consolidation is neither high enough nor sustainable in the long term to remove the great fiscal and financial risks looming over Serbia. The existing fiscal consolidation has not eliminated, but only slightly decreased, indeed postponed the risk of state bankruptcy. It is apparent by the budget deficit still being high and the public debt incessantly growing. Along with it, the amount of funds Serbia is paying for interest is growing, as well. In 2015 it amounted to ca. 4.2% of the GDP, whereas, for example, Greece allocated around 3.5% of its GDP for the same purpose.[10] Instead of intensifying austerity and thus consolidating public finances, the government would – by raising pensions and salaries – undermine the consolidation of public finances, which would not only increase the country’s risk of going bankrupt, but diminish the probability of introducing harsher austerity measures again as a means to forestall such a dire outcome.

Conclusion

The basic problem of Serbia’s economy is low economic growth, practically marked by years of stagnation, which has increased the problems of deficit, debt or low employment rates, or even caused them in the first place. Faster development could be achieved only by means of swift reform that would rely on the improvement of the business environment, rule of law and downsizing of the public sector. However, there is no such reform agenda.

In light of the stagnant economy, fiscal problems are coming to the forefront. They consist of high state expenditure which is partially financed by indebtedness, but also of irrational utilization of loans taken, which are being used as a means for buying the social peace, instead for investments – for example, in infrastructure. Serbia is taking on debt that exceeds its capability to service it in the long run, while using the funds irrationally. And when circumstances do force them to somewhat limit such dangerous policies, Serbian authorities do so belatedly and insufficiently – they aim to revoke even such modest austerity measures as soon as possible and to return to populist policies.

It is a high-risk policy that has become habitual. With it intact, the risk of bankruptcy remains high and can be activated by different occurrences, such as a rise in the price of money and taking on loans in the world market or a deeper recession at home; or possibly by the creditors’ mistrust in Serbia’s capability to service its public debt once it surpasses 80% or 90%, or by the crisis which will be caused by non-performing loans in the banking sector. It may be triggered by something else, something that at this point is not conceivable as an acute problem.

A policy of such risk cannot be pursued long without paying the adequate price for it – therefore, the period awaiting Serbia could be described as “years of living dangerously“. In less than 40 years, Serbia could face its fourth bankruptcy, three of which (1994, 2001, ?) in its own name, one as part of the Socialist Federal Republic of Yugoslavia (1983). Even though the circumstances of those events were different, as well as the magnitudes of the respective bankruptcies, they all have excessive state expenditure as a common trait. In late 1983, SFRY could not afford to take on any more debt, therefore resorting to a debt default, import limitations and restrictions in the procurement of even the basic commodities. The second bankruptcy came along with the 1992-1994 hyperinflation. This was a result of the state’s tendency to spend much more than it was available to it and since, due to the sanctions there was no possibility to borrow abroad, the only device left was the printing press as a source of lacking money, resulting in hyperinflation and breakdown of the economy and public finances. Finally, following the political changes in late 2000, Serbia faced the incapability to service its debt which had surpassed 200% of the GDP. A solution was found partially through debt write-off and restructuring, respectively. Overcoming bankruptcy and easing of the debt burden were aided by Serbia’s fast economic growth at the time, as well as by the creditors’ good will – both elements lacking today. Despite the difficulty in anticipating circumstances of a potential future bankruptcy of the country, it is not in the interest of Serbia’s citizens and should be avoided, even if harsher austerity measures than the present ones are the only way toward achieving this.

The author is a professor of economics from Belgrade.

Translation: Milan Bogdanović

* Quotet bibliography is attached to this article.

[1] Sum of the balance of trade, net primary income and cash payments. (Suma trgovinskog bilansa, neto primarnog dohotka I gotovinskih plaćanja)

[2] Prokopijević 2014

[3] Ministry of Finance 2015a, p. 17.

[4]Since the beginning of 2014 until mid-2015, the employment rate has increased by up to 240,000 persons which is more difficult to explain than the 160,000 increase, as it resembles occurrences amidst an economic boom, which is not the case here.

[5] Ministry of Finance 2015c, p. 41

[6] Fiscal Council 2015a, p.1, 3; 2015b, p. 1,10.

[7] Quarterly Monitor Vol. 40, p. 41.

[8] More effective collection of VAT is almost exclusively a result of increased tax repression, i.e. control by the Tax Administration and imposition of more penalties. Once the repression weakens, i.e. returns to its usual level, which is inevitable, the collection of VAT will diminish, too.

[9] See e.g. “Positive Assessment by the IMF“, Blic daily, September 1 2015.

[10] This is due to the fact that the Greek debt (incidentally, more than double as high in relation to its GDP compared to the Serbian debt) is stretched out over a longer period, with lower interest rates.

{kind=link}

{kind=link}

{kind=link}

{kind=link}